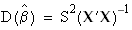

Parameter Dispersion (Variance-Covariance) Matrix

The

dispersion matrix for the parameter estimates

is the matrix

, where

is the covariance of

and

. The dispersion matrix is calculated according to the formula

where S

2 is the estimated variance, as defined above, and

X and

are the regression matrix and its transpose, respectively.

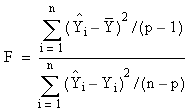

Significance of the Model (Overall F Statistic)

The

overall F statistic is a statistic for testing the null hypothesis

β1 =

β2 = ... =

βp – 1 = 0. It is defined by the equation:

where

This statistic follows an F distribution with (p-1) and (n-p) degrees of freedom.

p-Value

The p-value is the probability of seeing the value of the F statistic for a given linear regression if the null hypothesis:

β0 = β1 = ... = βp – 1 = 0

is true.

Critical Value

The critical value of the F statistic for a specified significance level, α , is the value, v, of the F statistic such that if the F statistic calculated for the multiple linear regression is greater than v, we reject the hypothesis β1 = β2 = ... = βp – 1 = 0 at the significance level α.