- java.lang.Object

-

- com.imsl.math.QuadraticProgramming

-

public class QuadraticProgramming extends Object

Solves the convex quadratic programming problem subject to equality or inequality constraints.Class

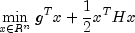

QuadraticProgrammingis based on M.J.D. Powell's implementation of the Goldfarb and Idnani dual quadratic programming (QP) algorithm for convex QP problems subject to general linear equality/inequality constraints (Goldfarb and Idnani 1983); i.e., problems of the form

subject to

given the vectors

,

,  , and

g, and the matrices H,

, and

g, and the matrices H,  ,

and

,

and  . H is required to be

positive definite. In this case, a unique x solves the

problem or the constraints are inconsistent. If H is not

positive definite, a positive definite perturbation of H

is used in place of H. For more details, see Powell

(1983, 1985).

. H is required to be

positive definite. In this case, a unique x solves the

problem or the constraints are inconsistent. If H is not

positive definite, a positive definite perturbation of H

is used in place of H. For more details, see Powell

(1983, 1985).If a perturbation of H,

,

is used in the QP problem, then

,

is used in the QP problem, then

also should be used in the definition of

the Lagrange multipliers.

also should be used in the definition of

the Lagrange multipliers.If the constraints are infeasible an exception is thrown. See Example 3 where the exception is caught and printed.

-

-

Nested Class Summary

Nested Classes Modifier and Type Class and Description static classQuadraticProgramming.InconsistentSystemExceptionThe system of constraints is inconsistent.static classQuadraticProgramming.NoLPSolutionExceptionNo solution for the LP problem with h = 0 was found byDenseLP.static classQuadraticProgramming.ProblemUnboundedExceptionThe object value for the problem is unbounded.static classQuadraticProgramming.SolutionNotFoundExceptionA solution was not found.

-

Field Summary

Fields Modifier and Type Field and Description static doubleEPSILON_SMALLThe smallest relative spacing for doubles.

-

Constructor Summary

Constructors Constructor and Description QuadraticProgramming(double[][] h, double[] g, double[][] aEquality, double[] bEquality, double[][] aInequality, double[] bInequality)Solve a quadratic programming problem.

-

Method Summary

Methods Modifier and Type Method and Description double[]getDual()Returns the dual (Lagrange multipliers).doublegetOptimalValue()Returns the optimal value.double[]getSolution()Returns the solution.booleanisNoMoreProgress()Returns true if due to computer rounding error, a change in the variables fail to improve the objective function.

-

-

-

Field Detail

-

EPSILON_SMALL

public static final double EPSILON_SMALL

The smallest relative spacing for doubles.- See Also:

- Constant Field Values

-

-

Constructor Detail

-

QuadraticProgramming

public QuadraticProgramming(double[][] h, double[] g, double[][] aEquality, double[] bEquality, double[][] aInequality, double[] bInequality) throws QuadraticProgramming.InconsistentSystemException, QuadraticProgramming.ProblemUnboundedException, QuadraticProgramming.NoLPSolutionException, QuadraticProgramming.SolutionNotFoundExceptionSolve a quadratic programming problem.- Parameters:

h- is square array containing the Hessian. It must be positive definite.g- contains the coefficients of the linear term of the objective function.aEquality- is a rectangular matrix containing the equality constraints. It can be null if there are no equality constraints.bEquality- contains the right-side of the equality constraints. It can be null if there are no equality constraints.aInequality- is a rectangular matrix containing the inequality constraints. It can be null if there are no inequality constraints.bInequality- contains the right-side of the inequality constraints. It can be null if there are no inequality constraints.- Throws:

QuadraticProgramming.InconsistentSystemException- if the system of constraints is inconsistent and there is no solution.QuadraticProgramming.ProblemUnboundedExceptionQuadraticProgramming.NoLPSolutionExceptionQuadraticProgramming.SolutionNotFoundException

-

-

Method Detail

-

getDual

public double[] getDual()

Returns the dual (Lagrange multipliers).

-

getOptimalValue

public double getOptimalValue()

Returns the optimal value.- Returns:

- a

double, the optimal value.

-

getSolution

public double[] getSolution()

Returns the solution.

-

isNoMoreProgress

public boolean isNoMoreProgress()

Returns true if due to computer rounding error, a change in the variables fail to improve the objective function. Usually the solution is close to optimum.

-

-