ACCR_INT_MAT Function (PV-WAVE Advantage)

Evaluates the interest which has accrued on a security that pays interest at maturity.

Usage

result = ACCR_INT_MAT(issue, maturity, coupon_rate, par_value, basis)

Input Parameters

issue—The date on which interest starts accruing. For a more detailed discussion on dates see Chapter 8, Working with Date/Time Data in the PV‑WAVE User’s Guide.

maturity—The date on which the bond comes due, and principal and accrued interest are paid. For a more detailed discussion on dates see Chapter 8, Working with Date/Time Data in the PV‑WAVE User’s Guide.

coupon_rate—Annual interest rate set forth on the face of the security; the coupon rate.

par_value—Nominal or face value of the security used to calculate interest payments.

basis—The method for computing the number of days between two dates. It should be either 0, 1, 2, 3 or 4.

0—Actual/Actual

1—US (NASD) 30/360

2—Actual/360

3—Actual/365

4—European 30/360

Returned Value

result—The interest which has accrued on a security that pays interest at maturity. If no result can be computed, NaN is returned.

Input Keywords

Double—If present and nonzero, double precision is used.

Discussion

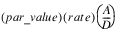

Function ACCR_INT_MAT computes the accrued interest for a security that pays interest at maturity:

In the above equation, A represents the number of days starting at issue date to maturity date and D represents the annual basis.

Example

In this example, ACCR_INT_MAT computes the accrued interest for a security that pays interest at maturity using the US (NASD) 30/360 day count method. The security has a par value of $1,000, the issue date of October 1, 2000, the maturity date of November 3, 2000, and a coupon rate of 6%.

issue = VAR_TO_DT(2000, 10, 1)

maturity = VAR_TO_DT(2000, 11, 3)

rate = .06

par = 1000.

basis = 1

PRINT, ACCR_INT_MAT(issue, maturity, rate, par, basis)

; PV-WAVE prints: 5.33333

Version 2017.0

Copyright © 2017, Rogue Wave Software, Inc. All Rights Reserved.