model—Four element array containing the numbers p, q, s, d of the ARIMA  , model the outlier free series is following.

, model the outlier free series is following.

, model the outlier free series is following., model the outlier free series is following. :

:

, can be computed as:

, can be computed as:

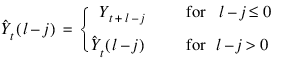

is done in two steps:

is done in two steps:

, can be computed recursively as:

, can be computed recursively as:

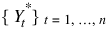

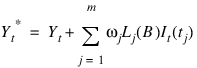

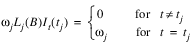

by adding the multiple outlier effects to the forecasts for {Yt}.

by adding the multiple outlier effects to the forecasts for {Yt}.Outlier | Formula |

Innovational outliers (IO) |  |

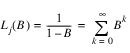

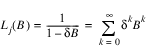

Additive outliers (AO) | Lj(B) = 1 |

Level shifts (LS) |  |

Temporary changes (TC) |  |

Outlier | Formula |

Innovational outliers (IO) |  |

Additive outliers (AO) |  |

Level shifts (LS) |  |

Temporary changes (TC) |  |

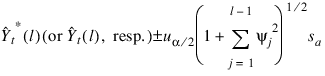

can be computed easily.

can be computed easily. and Yt+1 are given by:

and Yt+1 are given by:

is the 100(1 – α/2) percentile of the standard normal distribution,

is the 100(1 – α/2) percentile of the standard normal distribution,  is an estimate of the variance

is an estimate of the variance  of the random shocks (returned from TS_OUTLIER_IDENTIFICATION), and the ψ weights {ψj} are the coefficients in:

of the random shocks (returned from TS_OUTLIER_IDENTIFICATION), and the ψ weights {ψj} are the coefficients in:

time_series = [ $

41.67 , 41.67 , 42.0752144, 42.6123962, $

43.6161919, 42.1932831, 43.1055450, 44.3518715, $

45.3961258, 45.0790215, 41.8874397, 40.2159805, $

40.2447319, 39.6208458, 38.6873589, 37.9272423, $

36.8718872, 36.8310852, 37.4524879, 37.3440933, $

37.9861374, 40.3810501, 41.3464622, 42.6495285, $

42.6096764, 40.3134537, 39.7971268, 41.5401535, $

40.7160759, 41.0363541, 41.8171883, 42.4190292, $

43.0318832, 43.9968109, 44.0419617, 44.3225212, $

44.6082611, 43.2199631, 42.0419197, 41.9679718, $

42.4926224, 43.2091255, 43.2512283, 41.2301674, $

40.1057358, 40.4510574, 41.5329170, 41.5678177, $

43.0090141, 42.1592140, 39.9234505, 38.8394127, $

40.4319878, 40.8679352, 41.4551926, 41.9756317, $

43.9878922, 46.5736389, 45.5939293, 42.4487762, $

41.5325394, 42.8830910, 44.5771217, 45.8541985, $

46.8249474, 47.5686378, 46.6700745, 45.4120026, $

43.2305107, 42.7635345, 43.7112923, 42.0768661, $

41.1835632, 40.3352280, 37.9761467, 35.9550056, $

36.3212509, 36.9925880, 37.2625008, 37.0040665, $

38.5232544, 39.4119797, 41.8316803, 43.7091446, $

42.9381447, 42.1066780, 40.3771248, 38.6518707, $

37.0550499, 36.9447708, 38.1017685, 39.4727097, $

39.8670387, 39.3820763, 38.2180786, 37.7543488, $

37.7265244, 38.0290642, 37.5531158, 37.4685936, $

39.8233147, 42.0480766, 42.4053535, 43.0117416, $

44.1289330, 45.0393829, 45.1114540, 45.0086479, $

44.6560631, 45.0278931, 46.7830849, 48.7649765, $

47.7991905, 46.5339661, 43.3679199, 41.6420822, $

41.2694893, 41.5959740, 43.5330009, 43.3643608, $

42.1471291, 42.5552788, 42.4521446, 41.7629128, $

39.9476891, 38.3217010, 40.5318718, 42.8811569, $

44.4796944, 44.6887932, 43.1670265, 41.2226143, $

41.8330154, 44.3721924, 45.2697029, 44.4174194, $

43.5068550, 44.9793015, 45.0585403, 43.2746620, $

40.3317070, 40.3880501, 40.2627106, 39.6230278, $

41.0305252, 40.9262009, 40.8326912, 41.7084885, $

42.9038048, 45.8650513, 46.5231590, 47.9916115, $

47.8463135, 46.5921936, 45.8854408, 45.9130440, $

45.7450371, 46.2964249, 44.9394569, 45.8141251, $

47.5284042, 48.5527802, 48.3950577, 47.8753052, $

45.8880005, 45.7086983, 44.6174774, 43.5567932, $

44.5891113, 43.1778679, 40.9405632, 40.6206894, $

41.3330421, 42.2759552, 42.4744949, 43.0719833, $

44.2178459, 43.8956337, 44.1033440, 45.6241455, $

45.3724861, 44.9167595, 45.9180603, 46.9077835, $

46.1666603, 46.6013489, 46.6592331, 46.7291603, $

47.1908340, 45.9784355, 45.1215782, 45.6791115, $

46.7379875, 47.3036957, 45.9968834, 44.4669495, $

45.7734680, 44.6315041, 42.9911766, 46.3842583, $

43.7214432, 43.5276833, 41.3946495, 39.7013168, $

39.1033401, 38.5292892, 41.0096245, 43.4535828, $

44.6525154, 45.5725899, 46.2815285, 45.2766647, $

45.3481712, 45.5039482, 45.6745682, 44.0144806, $

42.9305000, 43.6785469, 42.2500534, 40.0007210, $

40.4477005, 41.4432716, 42.0058670, 42.9357758, $

45.6758842, 46.8809929, 46.8601494, 47.0449791, $

46.5420647, 46.8939934, 46.2963371, 43.5479164, $

41.3864059, 41.4046364, 42.3037987, 43.6223717, $

45.8602371, 47.3016396, 46.8632469, 45.4651413, $

45.6275482, 44.9968376, 42.7558670, 42.0218239, $

41.9883728, 42.2571678, 44.3708687, 45.7483635, $

44.8832512, 44.7945862, 44.8922577, 44.7409401, $

45.1726494, 45.5686874, 45.9946709, 47.3151054, $

48.0654068, 46.4817467, 42.8618279, 42.4550323, $

42.5791168, 43.4230957, 44.7787971, 43.8317108, $

43.6481781, 42.4183960, 41.8426285, 43.3475227, $

44.4749908, 46.3498306, 47.8599319, 46.2449913, $

43.6044006, 42.4563484, 41.2715340, 39.8492508, $

39.9997292, 41.4410820, 42.9388237, 42.5687332]

; We will use the first 280 to generate a forecast for the

; next 10 and test that forecast against these 10 actual

; observations.

forecast_actual = [42.6384087, 41.7088661, 43.9399033, $

45.4284401, 44.4558411, 45.1761856, $

45.3489113, 45.1892662, 46.3754730, $

45.6082802]

delta = 0.7

n_predict = 10

model = [2, 1, 1, 0]

result = TS_OUTLIER_IDENTIFICATION( $

model, time_series, $

Relative_Error=1.0e-4, $

Num_Outliers=num_outliers, $

Residual=residual, $

Outlier_Statistics=outlier_stat, $

Omega_Weights=omega, $

Arma_Param=parameters, $

Res_Sigma=res_sigma, $

Aic=aic)

PRINT, "ARMA parameters:"

PRINT, parameters, Format='(F11.6)'

PRINT, ''

PRINT, num_outliers, Format="('Number of outliers: ', I1)"PRINT, ''

PRINT, "Outlier statistics:"

PRINT, "Time point Outlier type"

FOR i=0L, num_outliers-1 DO $

PRINT, outlier_stat(i,0), outlier_stat(i,1), $

Format="(I6, 10X, I3)"

PRINT, ''

PRINT, res_sigma, Format="('RSE: ', F11.6)"PRINT, aic, Format="('AIC: ', F11.6)"PRINT, ''

; collect the output from the TS_OUTLIER_IDENTIFICATION call

; and arrange it for the call to TS_OUTLIER_FORECAST

series = FLTARR(N_ELEMENTS(time_series),2)

series(*,0) = time_series

series(*,1) = residual

forecast = TS_OUTLIER_FORECAST( $

series, $

outlier_stat, omega, delta, $

model, parameters, n_predict, $

Out_Free_Forecast=outfree_forecast)

forecast_table = FLTARR(n_predict,4)

PRINT, "** " + $

"Forecast Table for Outlier Contaminated Series **"

PRINT, "Orig. Series Forecast Prob. Limits PSI Weights"

FOR i=0L, n_predict-1 DO $

PRINT, forecast_actual(i), forecast(i,0), $

forecast(i,1), forecast(i,2), $

Format='(F10.4, 3F13.4)'

PRINT, ''

PRINT, "****** " + $

"Forecast Table for Outlier Free Series ******"

PRINT, " Outlier"

PRINT, " Free Series Forecast Prob. Limits PSI Weights"

FOR i=0L, n_predict-1 DO BEGIN & $

PRINT, forecast_actual(i), outfree_forecast(i,0), $

outfree_forecast(i,1), outfree_forecast(i,2), $

Format='(F10.4, 3F13.4)' & $

ENDFOR

ARMA parameters:

8.891920

0.944060

-0.150423

-0.558918

Number of outliers: 2

Outlier statistics:

Time point Outlier type

150 2

200 1

RSE: 1.004306

AIC: 1323.617554

** Forecast Table for Outlier Contaminated Series **

Orig. Series Forecast Prob. Limits PSI Weights

42.6384 43.6852 1.9684 1.5030

41.7089 43.8266 3.5535 1.2685

43.9399 44.0516 4.3430 0.9714

45.4284 44.2428 4.7453 0.7263

44.4558 44.3895 4.9560 0.5395

45.1762 44.4992 5.0685 0.4001

45.3489 44.5807 5.1293 0.2966

45.1893 44.6411 5.1624 0.2198

46.3755 44.6859 5.1805 0.1629

45.6083 44.7191 5.1904 0.1207

****** Forecast Table for Outlier Free Series ******

Outlier

Free Series Forecast Prob. Limits PSI Weights

40.1384 41.9598 1.9684 1.5030

39.2089 42.1012 3.5535 1.2685

41.4399 42.3262 4.3430 0.9714

42.9284 42.5174 4.7453 0.7263

41.9558 42.6641 4.9560 0.5395

42.6762 42.7738 5.0685 0.4001

42.8489 42.8553 5.1293 0.2966

42.6893 42.9157 5.1624 0.2198

43.8755 42.9605 5.1805 0.1629

43.1083 42.9937 5.1904 0.1207